Public liability insurance for painters is essential protection for you, the homeowner, covering costs if your property is accidentally damaged or someone is injured during your painting project. Hiring a painter without it means you could be personally liable for accidents.

If you're comparing painting quotes right now, insurance is one of the easiest things to overlook and one of the hardest things to fix after something goes wrong. A sharp price, a quick start date, and a friendly promise to “take care of it” don't help much if paint lands on a neighbour's car, a visitor trips over drop sheets, or exterior work on a tall weatherboard home falls outside the painter's policy.

In Melbourne, this matters even more. Many homes have tricky access, older surfaces, heritage features, tight apartment rules, or outdoor areas close to boundaries. That means public liability insurance painters carry isn't just a box-ticking detail. It's a practical measure that protects your property, your finances, and your ability to get a problem sorted properly.

Table of Contents

- What Public Liability Insurance Actually Covers

- Decoding Policy Limits From $5M to $20M

- How to Verify a Painter's Insurance Certificate

- Red Flags and Common Policy Exclusions

- Your Checklist for Hiring an Insured Painter

- Frequently Asked Questions about Painting Insurance

- What happens if I hire an uninsured painter and they damage my property?

- Is insurance more important for exterior painting than interior painting?

- Does public liability insurance cover peeling paint after a year?

- Should apartment owners ask for anything extra?

- What about heritage homes and older Melbourne properties?

- Is a Certificate of Currency enough on its own?

What Public Liability Insurance Actually Covers

Public liability insurance painters carry is there for accidental damage and third-party injury. For a homeowner, that means the policy is meant to respond when a normal painting job causes an unintended problem, not when the painter delivers poor workmanship.

Think of it a bit like car insurance. If someone accidentally hits your parked car, insurance is there for the accident. If they do a sloppy repair job on your bumper, that becomes a workmanship issue. Painting works the same way.

The two main things it protects

The first part is property damage. On a house painting project, that can include paint spilled on timber floors, overspray on glass, damage to a driveway, or a ladder scraping a rendered wall. On exterior painting, it can extend to damage outside the immediate work area, which is why boundary fences, cars, paving, windows, and garden features all matter.

The second part is third-party injury. If a visitor, neighbour, tenant, or delivery driver trips over equipment or is injured around the work area, public liability is the policy that should respond.

Practical rule: If the issue involves accidental physical damage or bodily injury during the job, public liability is the first policy to ask about.

That distinction matters because homeowners often assume “fully insured” means every problem is covered. It doesn't.

What it usually does not cover

Public liability generally doesn't cover faulty workmanship. If a painter skips preparation, applies the wrong system, leaves flashing, or the finish fails because the work was done badly, that usually sits outside public liability. That's where a written workmanship warranty matters.

It also doesn't automatically solve every dispute about specifications. Australian painting policies commonly exclude subcontractor-caused damage, height-related incidents above stated limits, and lead-based paint disposal. They also need to be checked against professional indemnity requirements, because if a paint colour doesn't match the agreed specification, professional liability may cover the repaint cost while general liability does not, as explained by LandesBlosch's guide to painting contractor liability insurance.

For homeowners, the practical takeaway is simple:

- Accidental spill or breakage: usually a public liability issue

- Someone hurt on site: usually a public liability issue

- Wrong colour from a documented spec: may require professional indemnity, not public liability

- Peeling caused by poor prep: usually a workmanship issue, not a public liability issue

If you want a broader understanding of how liability protection works when a business causes harm through what it supplies, this plain-English explanation of protecting Aussie businesses from faulty products is also useful. It helps clarify why different insurance types exist and why one policy rarely covers every kind of claim.

Public liability insurance is important, but it is only one layer of protection. Good painters also rely on clear written quotes, defined preparation, suitable coating systems, and a workmanship warranty.

That's especially relevant for interior painting, cabinet painting, bathroom and bathtub painting, and epoxy floor painting, where the finish specification matters just as much as accident cover.

Decoding Policy Limits From $5M to $20M

The coverage amount on a painter's policy tells you how seriously the business treats risk. It also tells you whether the policy is likely to fit the type of property you own.

In Australia, painters must hold minimum public liability cover ranging from $5 million to $20 million depending on the state and project scale, and Victoria requires at least $10 million for commercial work, rising to $20 million for high-risk jobs. The same verified industry data notes that the construction sector, including painting, accounted for 28% of workplace compensation claims, and property damage claims averaged $45,000 per event in the reported data set (Fact 1).

Why the number matters

A small unit repaint and a large weatherboard exterior don't create the same exposure. Neither does repainting a standard bedroom versus coating a garage floor, spraying an exterior near parked cars, or working around a heritage façade with hard-to-replace details.

A lower policy limit can still sound respectable to a homeowner. However, the essential question isn't whether the number sounds big. It's whether the number suits the job.

For Melbourne properties, higher limits become more relevant when the project includes:

- Heritage details: timber fretwork, decorative plaster, stained glass surrounds, or older lead-affected surfaces

- Apartment access: common property, lifts, basements, body corporate rules, and neighbouring residents

- Tight boundaries: overspray or accidental contact affecting a next-door fence, carport, or shared driveway

- Higher-risk systems: scaffolds, raised exterior work, epoxy coatings, and specialty finishes

A painter carrying $20 million in cover is usually signalling something important. They understand that one claim can involve more than a tin of paint on a carpet. It can involve multiple affected parties, legal costs, access issues, and repairs that spread well beyond the original work area.

Painter Insurance Coverage Levels Compared

| Coverage Level | Typical For | Potential Risk Gap for Homeowner |

|---|---|---|

| $5M | Smaller, lower-risk jobs where minimum cover may satisfy basic requirements | May feel thin for larger homes, tight boundaries, or jobs with multiple exposure points |

| $10M | Victorian commercial baseline and more established operations | Can still leave less margin on high-risk or more complex residential work |

| $20M | Higher-risk work and businesses taking broader risk management seriously | Stronger protection buffer for complex homes, apartments, heritage projects, and multi-party claims |

A higher limit doesn't prove quality by itself. It does show the painter has chosen to carry more financial protection if something goes wrong.

There's also a professionalism test hidden inside the number. Painters who work on pre-sale painting, apartment painting, exterior repainting, and occupied homes should already know what level of cover clients and property managers expect. If they hesitate when asked, or downplay the question, that's useful information.

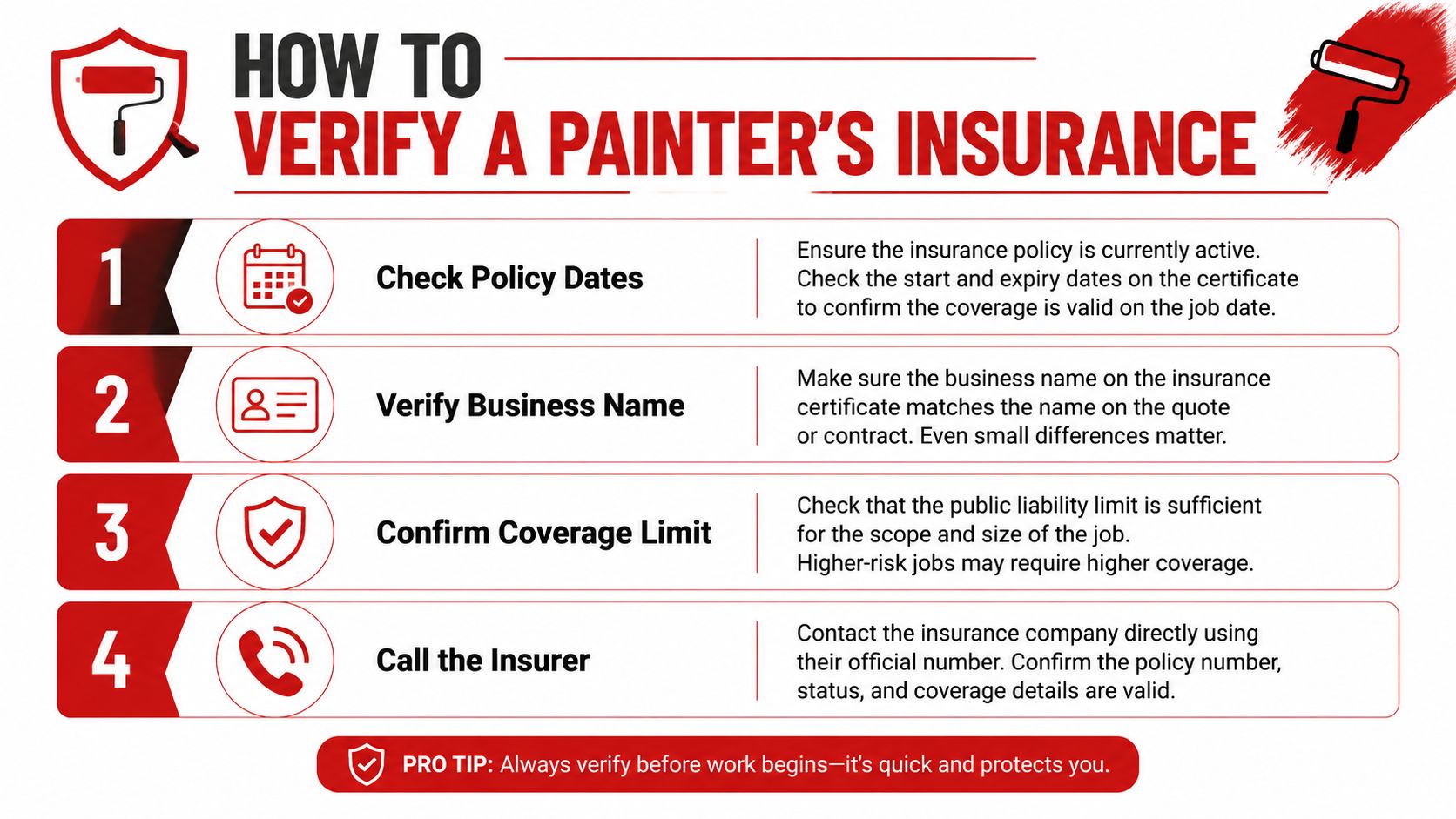

How to Verify a Painter's Insurance Certificate

Never rely on “yes, we're insured” over the phone. Ask for the Certificate of Currency before work starts, and check it against the quote.

Victoria's tighter verification culture didn't appear by accident. After the HIH collapse triggered Australia's public liability crisis, Victoria moved through tort reform and standardised insurance minimums that were adopted into VBA licensing by 2012, reinforcing the verification systems now expected in the trade (Fact 2).

What to check on the certificate

Three details matter immediately.

-

The insured business name

It should match the business issuing the quote and invoice. If the quote is from one name and the certificate shows another, ask why. Don't assume they're connected. -

The policy expiry date

A certificate that expired last month is not current cover. If your project runs over several weeks, make sure the policy stays active for the job period. -

The public liability limit

Confirm the amount of cover shown on the certificate. Don't settle for vague wording like “fully insured”.

Here's a helpful trade video on what to look for when checking cover:

A simple verification process

Most homeowners don't need to become insurance experts. They need a repeatable process.

- Ask early: Request the certificate with the written quote, not after you've paid a deposit.

- Match names carefully: Compare the legal business name on the quote, ABN details if supplied, and the insured party on the certificate.

- Check relevance: If the job is exterior painting on a double-storey house or apartment building, ask whether any height limitation applies.

- Call if unsure: If anything looks off, contact the insurer or broker listed on the document and ask them to confirm the policy is current.

If a painter becomes defensive when you ask for a Certificate of Currency, treat that as a warning sign, not a misunderstanding.

It also helps to compare their paperwork habits more broadly. A business that provides a detailed written quote, scope of preparation, paint system, timing, and insurance documentation usually runs jobs in a more organised way. If you're still comparing contractors, this guide on how to choose the right painter for your home is a useful next step.

For apartment painting and pre-sale makeovers, verification is even more important because there are more people affected by site activity. Owners corporations, tenants, neighbours, and agents all have a stake in how risk is managed.

Red Flags and Common Policy Exclusions

“Fully insured” can mean very little if the policy excludes the actual work being done. The gap usually appears in the fine print, not in the sales pitch.

Exclusions that matter on real painting jobs

Height restrictions are one of the biggest examples. A painter may be insured for general residential work but not for work above a specified height. That matters on Melbourne weatherboards, taller townhouses, apartment exteriors, stairwells, and any job needing scaffold access.

Subcontractor exclusions matter too. Some policies commonly exclude damage caused by subcontractors. If the business quoting your job brings in outside labour and those workers damage flooring, glazing, cabinetry, or common property, the claim path may become messy very quickly.

Lead-based paint disposal is another issue on older properties. Heritage and period homes often involve surfaces that need more caution. If disposal or contamination risk sits outside the policy, homeowners can end up dealing with a problem they never knew existed.

Some of the highest-risk painting jobs look ordinary at first glance. A front façade on an older Melbourne home can involve height, heritage materials, lead risk, foot traffic, and tight side access all at once.

Other gaps are less obvious but still important. Spray application can create overspray risk. Pre-sale work can create disputes about colour and finish representation. Decorative and specialty finishes can raise questions that fall outside basic accidental-damage cover.

Why aggregate limits can catch homeowners out

Policy limits don't only work one way. Standard public liability structures often split the cover between a per-occurrence limit and an aggregate limit, which is the total payout available across the policy period. For painters with multiple concurrent jobs, the aggregate can be exhausted, leaving later claims uncovered, as explained in Duncan Insurance's overview of liability insurance for painting contractors.

That matters most with businesses juggling several jobs at once. A homeowner may see a certificate and assume the full amount is available to them. In practice, part of that policy could already have been exposed elsewhere.

Watch for these red flags:

- No clear answer on height limits: risky for exterior and apartment work

- Vague wording around who is covered: especially if crews change during the project

- No discussion of subcontractors: common source of confusion after an incident

- No distinction between accident cover and workmanship: often a sign the painter doesn't understand their own policy

- No written process for protection and clean-up: insurance helps after damage, but prevention still matters more

For interior painting, cabinet painting, bathroom coatings, and epoxy floor systems, planning and documentation count. The best operators don't just carry cover. They build the job to reduce the chance of needing it.

Your Checklist for Hiring an Insured Painter

If you want to avoid problems, treat insurance as part of the hiring decision, not as paperwork to collect at the end. A good painter should be able to answer direct questions without hesitation.

Questions worth asking before you sign

Use this checklist before approving a quote:

-

Can I see your current Certificate of Currency?

Ask for it with the quote, not after deposit payment. -

Does the insured name match the business on the quote and invoice?

If not, ask for a clear explanation in writing. -

What is your public liability cover amount?

Don't accept “we're covered”. Ask for the actual figure shown on the certificate. -

Does your policy cover everyone working on my property?

This matters if the business uses a team, temporary labour, or subcontractors. -

Are there any height restrictions relevant to my job?

Essential for exterior painting, apartment work, stair voids, and scaffold access. -

Are there exclusions for lead-related work or disposal?

Important on older Melbourne homes and heritage-style properties. -

If the colour or finish is wrong against the written quote, what covers that?

This helps separate public liability from professional indemnity and workmanship obligations. -

What warranty do you provide for the work itself?

Insurance does not replace a workmanship warranty.

Homeowner shortcut: If a painter can't explain their cover in plain English, don't expect them to handle a claim smoothly when stress is high.

What good documentation looks like

Good documentation usually arrives as a package, not a scramble. You should expect a written quote, a clear scope, preparation details, products or paint systems, scheduling notes, and current insurance documents.

This matters even more on higher-stakes residential work. Standard policies can have gaps for heritage elements, colour misrepresentation in pre-sale projects, latent paint defects, or improper disposal of lead-based paint from Victorian heritage properties. A $20 million policy is a strong starting point, but homeowners should still ask whether the cover addresses those higher-stakes risks (Fact 6).

A solid hiring file for your project should include:

| Item | Why it matters |

|---|---|

| Written quote | Defines what's included, excluded, and how surfaces will be prepared |

| Certificate of Currency | Confirms current public liability cover |

| Preparation notes | Shows whether sanding, patching, priming, masking, and protection are part of the job |

| Product system details | Important for bathrooms, cabinets, weatherboards, driveways, and epoxy floors |

| Warranty terms | Separates accidental damage cover from workmanship responsibility |

If you're comparing local contractors, a practical way to shortlist options is to start with painters who already present this material clearly. This list of Melbourne painters near you is a useful place to continue your comparison.

For homeowners, property managers, and agents, the point is simple. The cheapest quote can become the most expensive if the insurance is weak, expired, narrow, or poorly understood.

Frequently Asked Questions about Painting Insurance

What happens if I hire an uninsured painter and they damage my property?

You may end up chasing the business directly for repair costs, and if they can't pay, the problem can become yours. That's why proof of current cover matters before any work starts.

Is insurance more important for exterior painting than interior painting?

Both matter, but the risks differ. Exterior work often raises access and height issues. Interior work can involve expensive floors, furniture, joinery, benchtops, and occupied spaces with more foot traffic.

Does public liability insurance cover peeling paint after a year?

Usually not if the issue comes back to poor preparation, wrong product selection, or faulty workmanship. That's where a written workmanship warranty is important.

Should apartment owners ask for anything extra?

Yes. Ask whether the policy applies to work in common areas, access routes, lifts, basements, and higher-level work if relevant. Apartment jobs can affect neighbours and building management, not just your lot.

What about heritage homes and older Melbourne properties?

Ask specifically about exclusions relating to height, lead-based paint disposal, and delicate or high-value surfaces. Older homes often carry risks that don't appear on a basic repaint quote.

Is a Certificate of Currency enough on its own?

It's the starting point, not the whole answer. You also want a detailed written quote, a clear scope of preparation, and a workmanship warranty. If you want more practical homeowner guidance, Newline's painting FAQs are worth reading.

If you want a Melbourne painter who treats insurance, preparation, and documentation as essential standards, Newline Painting is a strong benchmark. Every project starts with a clear written quote and practical advice on scope, preparation, coatings, and scheduling, backed by $20 million public liability insurance and a 7-year workmanship warranty. If you're planning interior painting, exterior painting, apartment painting, pre-sale painting, cabinet refinishing, bathroom coatings, fence painting, or epoxy floor painting, you can request a free on-site quote and compare the paperwork properly before you commit.